比亚迪2025年报深度解读:净利润下滑19%背后,二代刀片电池让狼真的来了

比亚迪2025年年报显示营收8040亿、净利润326亿同比下降19%,但研发投入高达634亿。2026年3月发布的二代刀片电池与闪充技术被视为真正的转折点,或重塑纯电与插混的市场格局。本文深度解读比亚迪"两条腿齐步走"战略的底层逻辑与未来走向。

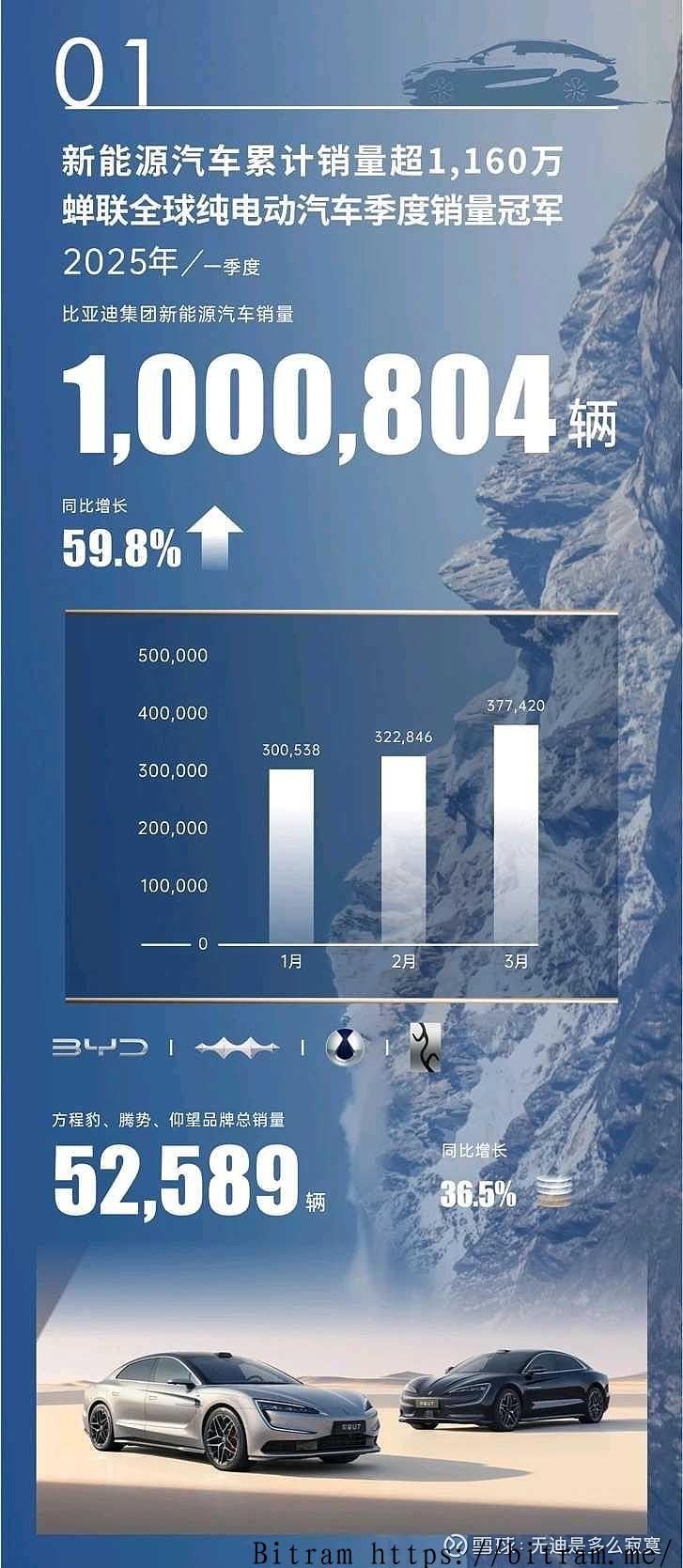

比亚迪近期发布的2025年年度报告,交出了一份喜忧参半的成绩单。全年营收突破8040亿元,同比增长3.5%,但归母净利润仅录得326.2亿元,同比下降19%。利润承压的背后,是比亚迪将634亿元重金押注于研发——这一数字在全球汽车行业中堪称罕见。超级e平台、第五代DM混动系统、天神之眼智驾方案……一项项技术发布频繁刷屏,但市场对"黑科技"的反应向来是雷声大、雨点小。真正让外界屏息的,是2026年3月5日亮相的二代刀片电池与超级闪充技术——这一次,狼是真的来了。

纯电与插混的"麻花"博弈

过去五年,比亚迪纯电与插混两条产品线的销量走势,活像一根缠绕的麻花,此消彼长、轮番反超。2021年纯电以54%微弱领先,2022年插混反超,2023年纯电再度夺回优势,2024年插混以58.5%的占比大幅领先,2025年则几乎打平——纯电225.6万辆、插混228.9万辆,近乎五五开。这种拉锯折射出一个客观现实:油价、充电桩覆盖率、碳酸锂价格等外部变量,持续左右消费者的购车决策。

比亚迪从未公开押注哪条技术路线更优,而是选择两线并举,哪边环境成熟就让哪边跑得更快。

这正是"两条腿、齐步走"策略的浅层逻辑——东边不亮西边亮。而更深层的逻辑则是:不赌风口,只管把技术做扎实、把用户痛点解决好,让市场自己给出答案。这一策略帮助比亚迪连续数年稳居全球新能源车销量冠军。

闪充落地,格局或将重塑

2026年开局,比亚迪销量数据颇为难看——纯电与插混分别同比下跌35%和36.7%。但这个数字未必是战略失效的信号,更可能是"持币待购"效应的集中爆发:大量潜在买家在二代刀片电池正式落地前选择观望,主动延迟消费决策。

二代刀片电池与最高1MW充电功率的超级e平台结合,有望大幅压缩充电时间、缓解里程焦虑,推动部分原本倾向于插混的消费者转投纯电阵营。但这并不意味着插混时代的终结。全球仍有大量地区充电基础设施薄弱,加之许多消费者对燃油车驾乘质感的留恋,插混在未来若干年内依然具备相当的市场空间。

值得关注的是,自2023年起,比亚迪整车销售毛利润已超越特斯拉——当年比亚迪整车毛利润率达21%,而特斯拉为17.1%。盈利能力的结构性改善,为持续高强度研发投入提供了底气。

净利润的短期下滑,掩盖不了比亚迪在技术积累与规模优势上的长期布局。二代刀片电池是否真能成为纯电普及的临界点,2026年的销量数据将是最直接的答案。

BYD 2025 Annual Report Analysis: Behind the 19% Profit Drop, the Next-Gen Blade Battery Changes Everything

BYD's recently published 2025 Annual Report presents a mixed picture. Full-year revenue reached 804 billion yuan, up 3.5% year-on-year, while net profit attributable to shareholders came in at 32.62 billion yuan — a decline of 19%. Behind the profit squeeze lies a record-breaking R&D commitment of 63.4 billion yuan, a figure rarely matched anywhere in the global auto industry. Breakthrough after breakthrough made headlines — the Super e-Platform, the 5th-generation DM hybrid system, the "Eye of God" intelligent driving solution — yet market responses often fell short of the hype. What truly caught the industry off guard was the second-generation Blade Battery and ultra-fast charging technology unveiled on March 5, 2026. This time, the wolf has really arrived.

The Twisting Race Between BEV and PHEV

Over the past five years, BYD's pure electric (BEV) and plug-in hybrid (PHEV) product lines have traded places in a dizzying pattern. Pure EVs led with 54% of BYD's NEV sales in 2021, only to be overtaken by PHEVs in 2022. BEVs clawed back ahead in 2023, PHEVs surged to 58.5% of total sales in 2024, and by 2025 the two were virtually neck and neck — 2.256 million BEVs versus 2.289 million PHEVs. This perpetual tug-of-war reflects a simple truth: external variables such as fuel prices, charging infrastructure coverage, and lithium carbonate price fluctuations continuously reshape consumer preferences.

BYD has never publicly bet on one technology path over the other. Instead, it runs both in parallel — whichever lane is clearer at any given moment gets to move faster.

This is the surface logic of BYD's "two legs, same stride" strategy — if one side dims, the other shines. The deeper logic is more disciplined: don't chase trends, just solve real problems with solid technology and let the market decide. This approach has kept BYD at the top of the global NEV sales rankings for consecutive years.

Fast Charging Goes Live — Could the Landscape Shift?

BYD's sales figures for the first two months of 2026 looked alarming — BEVs fell 35% year-on-year while PHEVs dropped 36.7%. Yet these numbers may not signal strategic failure. A more likely explanation is a concentrated "wait-and-see" effect: a large pool of potential buyers chose to delay purchases ahead of the second-gen Blade Battery's official availability.

The combination of the new Blade Battery and the Super e-Platform's peak charging power of up to 1 megawatt could dramatically cut charging times and ease range anxiety — potentially pulling some consumers who had settled on PHEVs back toward pure EVs. That said, the PHEV era is far from over. Charging infrastructure remains inadequate across many regions globally, and a significant share of drivers still value the familiar feel of combustion-assisted driving. PHEVs are likely to retain substantial market relevance for years to come.

Also worth noting: since 2023, BYD's gross margin on vehicle sales has surpassed Tesla's — BYD posted a 21% gross margin on vehicles that year, compared to Tesla's 17.1%. This structural improvement in profitability gives BYD the financial runway to sustain its aggressive R&D investment cycle.

The short-term dip in net profit should not obscure BYD's long-term positioning in technology depth and manufacturing scale. Whether the second-generation Blade Battery becomes the true inflection point for mass EV adoption is a question the 2026 sales data will answer most honestly.

发表评论