养老机构"爆雷"五步圈钱术:骗过民政、银行与老人的完整骗局链条

湖南多家民办养老机构相继"爆雷",老人退赔比例最低仅3%。本文拆解非法集资养老机构从披合法外衣、成立公司收钱、混用资金、抵押资产到庞氏崩盘的五步圈钱路径,揭示银行抵押权优先、行政监管缺位如何合力让老人血本无归。

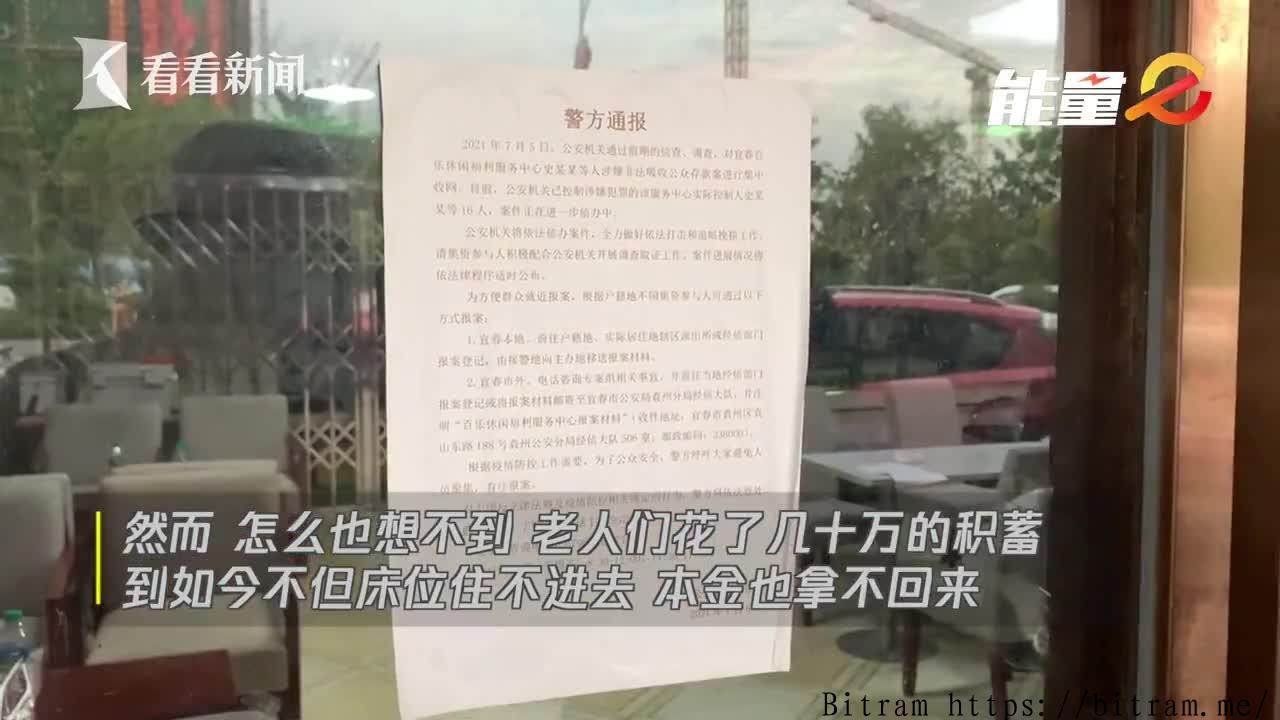

一场以"养老"为名的系统性金融骗局,正在湖南等地留下难以弥合的烂摊子。多家民办养老机构相继资金链断裂、老板锒铛入狱,然而老人们追回的养老钱,最少的只有本金的3%,多的也不过12%。这不是简单的"被骗",而是一套精心设计、多方配合、系统性收割老年群体的圈钱闭环。

拆解这类非法集资养老机构的运作模式,可以清晰看到五个环环相扣的步骤。理解这套路数,不仅是还原骗局,更是揭示监管漏洞何在。

五步圈钱:从合法外衣到庞氏崩盘

第一步:披上合法外衣。 骗局的起点往往是一张由民政部门颁发的"民办非企业单位"登记证书。负责人可能顶着"爱心大使""人大代表"的头衔,机构看起来正规、公益、有政府背书,天然具备信任感。

第二步:另立公司收钱。 骗局的核心结构是"两张皮"——一个非营利的养老公寓,对外承接政府补贴和公益形象;一个营利性的"XX老年服务公司",专门与老人签订养老服务合同,承诺年化8%至12%的高额回报。老人的钱,就从这一步流入了法律灰色地带。

第三步:资金混同挪用。 按规定,民办养老机构建设资金应来自合法融资或自有资本,而非向公众承诺收益的集资。但实际操作中,这一红线往往被忽视。老年人养老金集资缺乏有效监管,资金池完全由骗局操盘手掌控,一旦入场,老人几乎没有任何保障。

第四步:以房抵押套银行贷款。 用集资款建起的楼,再拿去抵押给银行,套出新一轮贷款,继续扩建、继续招揽新投资者。此时,这些资产已背负双重债务:老人的集资款和银行的贷款。而法律的天平,倾向银行——因为银行握有抵押权,老人的集资属于非法,毫无优先受偿保障。

第五步:庞氏崩盘,一地鸡毛。 养老公寓的正常运营收入根本覆盖不了高额利息,只能不断拆东墙补西墙,用新集资款偿还旧账。一旦新资金来源断绝,资金链瞬间崩塌。

爆雷之后:老人为何血本无归?

崩盘之后,老人面临的是三重困境。

- 银行优先受偿:司法拍卖资产时,持有抵押权的银行排在最前,老人几乎分不到任何补偿,部分案例中分配比例为零。

- 资产难以变现:部分养老公寓的土地为农村集体用地或租赁性质,根本无法办理正规产权证,"爆雷"后连拍卖都成问题。

- 行政追责无门:民政等部门的立场是:当年批准的是合法机构,没有批准非法集资,行政行为本身并无过错,与老人损失之间不存在直接因果关系。

湖南多家2019年前后爆雷的养老机构,老人实际拿回的比例最低仅为3%,最高也不过12%。

值得关注的是,长沙星城颐养院(原青松老年公寓)是少数例外——1118位老人的1.73亿元集资款得到100%退赔,成为行业中罕见的正向案例。这说明,结果并非无法改变,关键在于处置机制是否真正向受害者倾斜。

养老机构非法集资骗局暴露的,不只是个别骗子的恶意,更是"民非"与营利公司双轨并行、银行抵押与民间集资法律地位悬殊、行政监管事前缺位事后推责之间的系统性漏洞。在制度性修补到位之前,老年人面对"高息养老投资",最稳妥的选择仍然是:不碰。

The Five-Step Fraud Playbook Behind China's Exploding Elder Care Scams

A systematic financial fraud operating under the guise of "elderly care" has left a trail of devastation across Hunan Province and beyond. As multiple privately-run senior care facilities collapsed and their operators faced criminal prosecution, the elderly victims recovered as little as 3% of their principal — and no more than 12% in the best cases. This was no ordinary scam. It was a carefully engineered, multi-party system designed to systematically extract wealth from China's aging population.

Breaking down the mechanics of these illegal elder care fundraising schemes reveals five interlocking steps. Understanding this playbook is not just about reconstructing the fraud — it is about identifying exactly where regulatory oversight failed.

Five Steps from Legal Facade to Ponzi Collapse

Step 1: Dress up in legitimacy. Every scheme begins with a certificate of registration as a "private non-enterprise unit," issued by the civil affairs authority. Operators often carry titles like "Goodwill Ambassador" or "People's Congress Representative." The institution appears formal, charitable, and government-endorsed — a trusted face that lowers victims' guard.

Step 2: Set up a separate company to collect money. The structural core of the fraud is what insiders call the "two-skin" model: a non-profit senior care facility absorbs government subsidies and projects a public-interest image, while a separately registered, for-profit "elderly services company" signs contracts with residents and promises annual returns of 8% to 12%. It is at this step that elderly people's money crosses into a legal gray zone.

Step 3: Commingle and divert funds. Regulations require that construction funds for private care facilities come from legitimate financing or the operator's own capital — not from public fundraising with promised returns. In practice, this line was routinely ignored. Elder care investment funds operated without meaningful oversight, giving operators unchecked control over a pooled cash reserve with no protection for contributors.

Step 4: Mortgage assets to extract bank loans. Buildings constructed with residents' pooled money were then pledged as collateral to banks in exchange for new loans. The fresh capital funded further expansion and attracted even more investors. By this point, the assets carried double liabilities: the residents' pooled contributions and the bank debt. Under Chinese law, the balance tips decisively toward banks — they hold secured collateral rights, while the residents' contributions, being illegally solicited, carry no priority claim whatsoever.

Step 5: The Ponzi unravels. Operating revenue from the facility never came close to covering the high-interest obligations. Operators paid earlier investors using money raised from newer ones. The moment the flow of new funds dried up, the entire structure collapsed.

After the Collapse: Why Do Victims Walk Away with Almost Nothing?

Once the scheme implodes, elderly victims face a triple bind.

- Banks get paid first: In judicial asset auctions, secured creditors — the banks — stand at the front of the line. Elderly investors receive little to nothing. In some cases, their share of recovered assets is literally zero.

- Assets are difficult to liquidate: Many care facilities were built on rural collective land or leased land, making it impossible to obtain formal property title certificates. After collapse, even auctioning those assets becomes legally complicated.

- No administrative recourse: Civil affairs departments maintain that they approved a lawful institution, not an illegal fundraising operation, and that their regulatory conduct was procedurally sound — creating no direct legal liability toward victims.

Among the Hunan facilities that collapsed around 2019, recovery rates for elderly victims ranged from a low of just 3% to a high of only 12%.

One notable exception stands out. Changsha Xingcheng Yi Yang Yuan — formerly known as Qingsong Senior Apartments and once the largest private care facility in Changsha County — achieved a 100% restitution rate. All 173 million yuan collected from 1,118 elderly residents was fully returned. This case proves that outcomes are not fixed; what matters is whether the resolution mechanism is genuinely oriented toward protecting victims.

The elder care Ponzi fraud phenomenon exposes more than individual bad actors. It lays bare a set of systemic vulnerabilities: the legal gap between non-profit shell entities and their for-profit subsidiaries, the vast disparity in legal standing between secured bank creditors and unsecured elderly depositors, and a regulatory culture that approves operations upfront but deflects responsibility when they fail. Until these structural flaws are addressed, the safest advice for seniors facing "high-yield elderly care investment" opportunities remains unchanged: walk away.

发表评论