养老机构"爆雷"五步圈钱术:骗过民政、银行与老人的完整骗局链条

多家民办养老机构相继"爆雷",老人养老钱血本无归。本文揭示非法集资养老机构从披合法外衣、成立公司收钱、资金挪用、抵押套贷到庞氏崩盘的五步骗局链条,分析银行抵押权优先、老人追偿无门的制度困境,并探讨如何防范养老金融骗局。

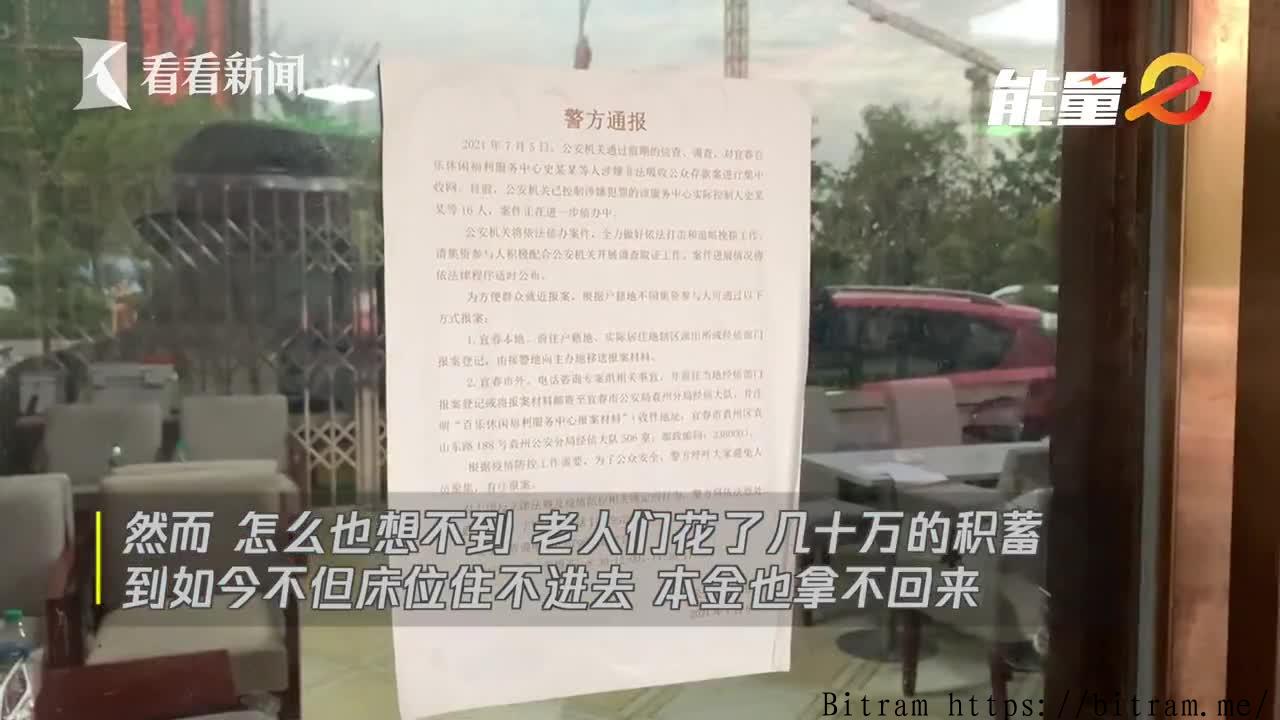

近年来,湖南多家民办养老机构相继"爆雷",数千名老人辛苦积攒的养老钱打了水漂。骗子落网了,房产被查封了,可老人实际拿回的退赔比例,低的只有3%,高的也不过12%。这场以"养老"为名的金融骗局,究竟是怎么运转的?又为何让民政部门、银行和普通集资人都难以脱身?

五步"圈钱":一套精心设计的骗局

这类非法集资养老机构的运作,往往遵循一套高度相似的路径。

第一步,披上合法外衣。 先由民政部门登记为"民办非企业单位",机构负责人往往顶着"爱心大使""人大代表"等光环,让人觉得"有政府背书、值得信赖"。

第二步,另立公司收钱。 在合法养老机构旁边,悄悄注册一家"XX老年服务有限公司",以公司名义与老人签合同,承诺年化8%至12%的高额回报,诱导老人大额"投资"。

第三步,资金混同挪用。 两个主体的钱混在一起使用,既无独立账户,也无第三方监管,老人的集资款随时可能被挥霍一空,却缺乏任何预警机制。

第四步,拿老人的钱抵押套贷。 用集资款建起的房产,再以公司名义抵押给银行,贷出新一笔资金——既用于扩大规模、吸引更多老人入局,也覆盖短期利息支出。这一操作使资产背负双重债务:银行享有法定抵押权,老人的集资却处于法律灰色地带。

第五步,庞氏崩盘。 当新的集资资金无法覆盖旧账的本息,资金链断裂,全面崩盘。

"爆雷"之后:银行先走,老人垫底

湘潭玉泉山庄被司法查封的9栋楼中,有8栋已抵押给银行。

这是整个骗局中最残酷的一幕。"爆雷"前夕,银行往往率先宣布贷款提前到期并提起诉讼;一旦进入资产拍卖程序,银行凭借抵押权优先受偿,老人分到的残余资产少之又少,有时甚至为零。

更棘手的是,部分资产的土地性质为农村集体土地或租赁用地,根本无法办理正式产权证,导致拍卖困难重重,最终可能无人接盘。而追责行政机关同样面临法律壁垒——民政部门当年批准的是合法养老资质,并未授权非法集资,行政责任与老人直接损失之间的因果关系难以认定。

这一困境揭示了养老金融监管的系统性漏洞:非营利机构与营利公司之间的"两张皮"操作,在现行监管框架下长期游走于灰色地带。

也有例外:100%退赔如何实现?

并非所有"爆雷"案例都以悲剧收场。长沙星城颐养院(原青松老年公寓)曾是长沙县最大民办养老机构,同样经历了崩盘,但1118位老人最终实现了100%全额退赔,共计1.73亿元。这一案例证明,在司法追缴力度足够、资产处置配合及时的前提下,最大限度保护老人权益并非不可能,关键在于政府介入的意愿与执行力。

防范养老金融骗局,核心在于识别"高息承诺+两层主体+无资金监管"三个危险信号。对于老年群体而言,凡是以养老服务为名、承诺固定高额回报的"投资"项目,都应高度警惕。监管层面,打通民政、金融、市场监管之间的信息壁垒,才能从源头堵住这类骗局的生存空间。

Five Steps of Elder Care Fraud: How Ponzi Schemes Deceived Regulators, Banks, and Retirees

In recent years, a wave of private elder care institutions in Hunan Province has collapsed, leaving thousands of retirees with little to nothing of their life savings. The perpetrators have been jailed, properties have been seized — yet the actual recovery rate for victims has ranged from as low as 3% to a mere 12%. How did this financial fraud, dressed up as "elder care," manage to deceive regulators, banks, and ordinary investors alike?

Five Steps to Fraud: A Carefully Engineered Scheme

These illegal fundraising operations tend to follow a strikingly consistent playbook.

Step 1: Put on a legal disguise. The scheme begins with registering a legitimate "private non-enterprise unit" with civil affairs authorities. Founders often carry titles like "Goodwill Ambassador" or "People's Congress Deputy," projecting an image of government endorsement and public trustworthiness.

Step 2: Set up a separate company to collect money. Alongside the registered non-profit, operators quietly incorporate a "XX Elder Care Services Co., Ltd." This for-profit entity signs contracts with elderly investors, promising annual returns of 8% to 12% — the hook that draws retirees into the trap.

Step 3: Commingle and misappropriate funds. Money flows freely between the two entities, with no independent accounts or third-party oversight. Investors' funds can be spent at will, with no early warning mechanism in place — a critical regulatory blind spot in elder care financial fraud cases.

Step 4: Use investors' assets as collateral for bank loans. Properties built with collected funds are mortgaged to banks under the company's name, generating fresh capital to expand operations, attract new investors, and service existing interest payments. This maneuver creates double liability on the same assets: banks hold legally recognized collateral, while elderly investors' claims remain in a legal gray zone.

Step 5: The Ponzi scheme collapses. When incoming funds can no longer cover the principal and interest owed to earlier investors, the cash flow breaks down entirely and the whole structure implodes.

After the Collapse: Banks Get Paid First, Retirees Get Almost Nothing

Of the nine buildings seized by courts at Xiangtan Yuquan Mountain Villa, eight had already been mortgaged to banks.

This is the cruelest turn in the entire saga. Just before the collapse, banks typically declare loans immediately due and file suit. Once assets enter the auction process, banks exercise their mortgage priority rights and claim the lion's share of proceeds, leaving retirees with scraps — or nothing at all.

The situation is further complicated by the nature of many properties: built on rural collective land or leased land, they cannot obtain formal title certificates, making them extremely difficult to auction and often impossible to sell. Holding administrative authorities accountable is equally fraught — civil affairs departments approved a legitimate care facility, not an illegal fundraising operation, making it hard to establish a direct causal link between regulatory failure and investor losses.

This predicament exposes systemic gaps in elder care financial oversight: the deliberate structural split between a non-profit institution and a for-profit company has long allowed operators to exploit the gray areas of China's regulatory framework.

One Exception: How 100% Repayment Was Achieved

Not every collapse ends in tragedy. Changsha Xingcheng Nursing Home — formerly Qingsong Senior Apartment, once the largest private elder care facility in Changsha County — also failed, but all 1,118 affected elderly investors ultimately received full repayment, totaling 173 million yuan. This case demonstrates that with sufficient judicial enforcement, proactive asset recovery, and strong government will, protecting victims' rights to the fullest extent is achievable.

Guarding against elder care financial fraud comes down to recognizing three red flags: high-yield promises, a dual-entity structure, and the absence of fund supervision. For retirees, any "investment" program tied to elder care services that guarantees fixed high returns warrants serious scrutiny. At the regulatory level, breaking down information silos between civil affairs, financial, and market oversight agencies is essential to closing off the structural loopholes that allow such schemes to thrive.

发表评论